By Michael Beyea Reagan

This post was originally published by the Gotham Center for New York City History

The 1975 New York City fiscal crisis gets lots of historical and political attention, and rightly so. It was a turning point not just in city history, but in the history of US political economy; the crisis helped change the course of the nation. The slow turn away from the social and deficit spending of Keynesianism and toward neoliberalism and austerity were accelerated by the collapse of financing in New York. In the spring and summer of 1975, when facing a citywide economic depression and failing bond markets, the city decided to cut its budget, impose austerity, and rely on a new fiscal logic to “save the city.” This paved the way for similar approaches in other cities, and by the end of the decade and into the Reagan presidency the policy of austerity was increasingly used at the local and federal levels.

Many historians have sought to understand the crisis, most recently Kim Phillips-Fein in her excellent Fear City: New York’s Fiscal Crisis and the Rise of Austerity Politics. Phillips-Fein deftly shows how the move to austerity was less about fiscal necessity and more of a political choice, one laden with the contingent crises and rightward political drift of banks and businesses in the 1970s. She cogently argues that budgets are political, moral documents, and that they pose “inescapably political questions,” rather than strictly “accounting ones” to politicians and the public.

Phillips-Fein is right, but a detailed look at the budgets of the city reveals something deeper. By historicizing city budgets we can see that deficits were at historic lows in the 1970s compared to the overruns at the height of the Keynesian period in the 1960s. This tells us that rather than fiscal necessity driving austerity in the 1970s, it must have been other considerations that changed the fate of the city. In 1975, New York faced a classical Keynesian crisis, a depression in the real economy and a market failure in municipal bond financing, but it was a crisis without a Keynesian response. Instead of the state spending money to weather the downturn and grow through the trough, as was done in the 1960s, the city implemented a harsh form of austerity that cut jobs and services to the bone.

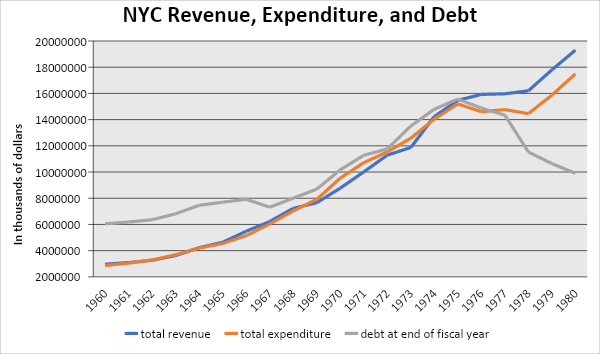

To better understand this turn, it helps to historicize city budgets. A quick look at previous decades reveals that New York debt in the 1970s was not at historic highs. A true measure of significance for deficit spending is debt to GDP ratios, but those numbers aren’t readily available for New York City. Instead, debt to revenue can show us the relative scale of deficits in historic terms for the period. Table one shows the relationship between city debt, revenue, and expenses as reported to the US Department of Commerce between 1960 and 1980.

As we can see, city debt to revenue ratios were twice as high in the 1960s as they were in the 1970s. In 1966 when the city faced a much-overlooked fiscal crisis, deficits were on the order of $6 billion, when incoming revenue was about $3 billion. These numbers reveal not only the importance of deficits through much of the Keynesian period of the 1960s, but they also raise questions about the scale and significance of the 1975 fiscal crisis and the need for austerity.

True, by 1974 and 1975 city debt had ballooned to $14 and $15 billion a year, respectively, a huge increase from a decade earlier. But those numbers were in line with the overall growth of the city budget, also roughly $15 billion in 1975. More importantly the ratio of debt to revenue was significantly decreased by the 1970s. These declining debt ratios are important because even with the budget gimmicks like “anticipatory note” offerings, inventive bookkeeping, and unknown cost overruns, overall, 1970s deficits were comparatively low. Deficits in the 1970s were real and growing in dollar value, but just a decade previous when deficits were much worse the city found solutions that didn’t involve drastic cuts to social services.

The causes of the fiscal crisis in 1975 was similar, but worse, compared to what the city experienced in the mid-1960s. One crushing factor was an economic depression in the real economy, which by the middle of the 1970s was acute. Like other cities experiencing deindustrialization New York was hemorrhaging firms, jobs, and residents. Between 1969 and 1976 New York City lost an average of 1000 industrial firms a year. That translated to a whopping decline of 500,000 manufacturing jobs from the city in that same period, pushing unemployment to ten percent and halving industrial employment in the city from its post-war high of just over one million. With the loss of jobs and firms came the loss of residents as New Yorkers fled the city by the thousands. In aggregate New York lost 11,000 housing units between 1970 and 1975 due to abandonment and demolition; by the end of the decade the city would lose close to one million residents.[1]

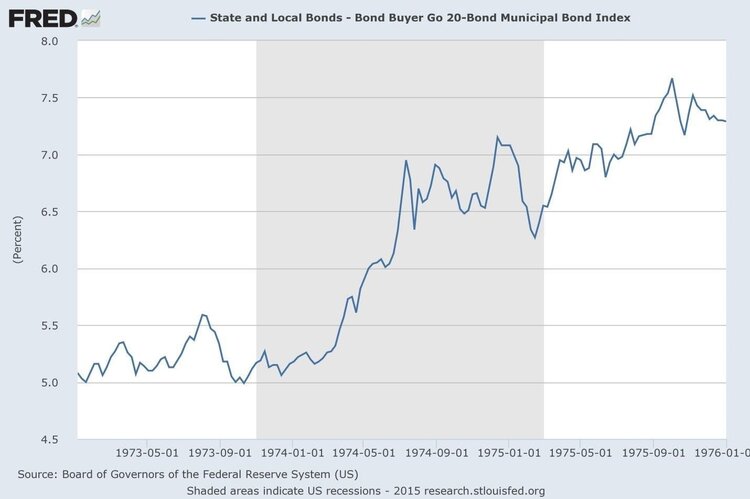

The other economic factor that compounded city finances was a historic failure of the municipal bond market. More than any other cause it is this market failure that drove the city to the fiscal brink in 1975. The OPEC crisis in 1973 started a chain reaction of economic forces that resulted in bond market failures and put a capital pinch on the city. The unexpected spike in oil prices contributed to unprecedented inflation, with a rate as high as twelve percent in the final months of 1974. Inflation is bad for consumer prices, pushing up city costs, but it is really bad for fixed rate investments like bonds. A modest return on a municipal bond with a yield of five percent could be a bedrock investment in normal economic conditions, but with double digit inflation in the mid-1970s investors were effectively losing upwards of five percent on city notes and other tax-exempt holdings. Average yield rates therefore soared from roughly five percent in 1973, to above seven and eight percent in 1975 and 1976. Before it was completely locked out of the market New York City offerings were being sold at rates higher than nine percent. These rate increases may not seem like much, but they were a three-fold increase over prices from a decade previous, and worse rates than what the bond market experienced during the Great Depression. With rates this high New York City and many other municipal notes were unsellable.

In 1974 and 1975 high yield rates on city notes were being offered to attract buyers, but a market for municipal bonds did not exist. Many large institutional investors like Wall Street banks had moved on from munis because inflation made returns on these investments so volatile and uncertain, and because they no longer needed the tax write-off that municipal bonds offered. The result was a market collapse; banks that once represented ninety percent of the market were selling their notes and not buying new ones. With an oversaturated market billions of dollars of municipal bonds went unsold through 1974 and into 1975. Sellers pulled their offerings, and analysts regularly commented that the market for municipal bonds was “virtually nonexistent,” and a “disaster area.” Don Reagan, Chairman and CEO of Merrill Lynch and future Treasury Secretary, called the municipal bond market in this period “a bloodbath.”

With a declining economy and no access to credit, by November of 1974 circumstances were overwhelming New York finances. That month, City Comptroller Harrison Goldin told the press that the city was struggling to pay its expenses. Goldin had been meeting with Wall Street financiers who shared his analysis of the problem. It was the collapse of the market and the lack of institutional investors that was driving New York from accessing credit. According to The New York Times which reported on Goldin’s meeting with bankers, Wall Street was reluctant to lend to New York, but “the reluctance does not arise from fears of a default – there are no doubts that the city can and will pay its debts.” Instead, it was fear of the market, particularly the “size and frequency of the borrowings, which are flooding an already overextended market for tax-exempt bonds.” Initially, no one worried about New York’s ultimate solvency; they worried about the market’s ability to provide credit given New York’s increasing needs.

Influenced by new economic thinking coming from Milton Friedman and others, by the spring of 1975 banks were using the crisis to leverage unprecedented requests on city finances to secure future funding. This meant up-to-the-day financial data on city expenses, information the city could not provide. By the summer, banks demanded significant and unprecedented cuts to spending, including key and cherished programs like free tuition at CUNY, the thirty-five cent subway fare, cuts to schools, hospital closures, and other reductions. The choice from bankers to target inflation at the cost of social programs and the wellbeing of regular New Yorkers was reflective of new economic thinking and social priorities from Wall Street.

The Ford administration was similarly influenced by the new economic thinking, and therefore also refused loans to the city in crucial months in 1975. Leading Ford Administration officials including Treasury Secretary William Simon, chief economic advisor Alan Greenspan, and Chief of Staff Donald Rumsfeld, all were enamored with the economics and philosophy of Friedman, Ayn Rand, and others. Although the Ford administration was eventually forced to reverse course and provide loans to the city, it was not before the city made major concessions and imposed a significant austerity program. Thus began the key period we know as the fiscal crisis for the city, which is historically notable not for the scale of city debts, but the scale of cuts in response.

By historicizing budgets and finance we can see that with a depression in the real economy, and lack of access to private credit, city budgets were in a bind. The depression was causing a decline in revenue and an increased need for social services. According to orthodox Keynesian policy, governments should rely on deficit spending to sustain the economy and grow through the trough. But without access to credit, New York couldn’t finance its expanding needs nor its regular operations. As a result we are confronted with a classic Keynesian crisis — economic depression and market failure — but with austerity as the proposed policy solution.

If our question then shifts to why New York moved to austerity instead of a traditional Keynesian approach to their crisis, we must look to answers other than fiscal profligacy. True, New York City employed numerous budgetary gimmicks and untraditional accounting to maintain their budgets. True, the city in the 1960s and early 1970s was expanding its welfare and public programs. But these budgetary problems, in historic terms, were not as significant as the fiscal crisis of the 1960s. In that decade increased social spending, new revenue streams, and greater efficiencies were all pursued to ensure New York’s solvency. By the 1970s banks were no longer interested in financing city spending partly for economic reasons, as banks didn’t need large volumes of tax-exempt holdings on their books any longer. But this was also political and cultural, when in the wake of the disruptive social movements of the 1960s banks and politicians were less committed to further expansions of social welfare.

Currently, New York City and State face significant budget shortfalls from the COVID-19 crisis. As we reflect on our moment, one when changing commitments to financing and social spending are afoot, it behooves us to look at the legacy of social spending in New York in the 1960s. What is evident is that our relationship to government debt is not as clear as the black and white numbers on an accounting ledger might indicate. Debt can be used in a number of ways that provide social benefit, even with the costs and risks associated with deficit financing. What the experience of New York City in the 1960s and 1970s shows us is that whether to run deficits or impose austerity is a choice. Indeed, a broader commitment to “social responsibility,” one that is not solely fiscal, can make sound social and economic policy. Given the scope of our own crises at a national scale, and much like New York in the Keynesian period, perhaps we can learn to accept deficits as the lesser of many evils.

Michael Beyea Reagan is an historian and writer based in Seattle. He is the author of Intersectional Class Struggle: Theory and Practice, and is working on a history of New York City debt called “The Budget is Everything.” He contributes to the Boston Review, Truthout, and other outlets.

[1] New York State Department of Commerce, New York State Business Fact Book; U.S. Department of Labor, Bureau of Labor Statistics, Employment, Hours, and Earnings, States and Areas, 1939-82: Vol. II, New Hampshire-Wyoming; Paul Cowan, “The Region In Summary,” New York Times, May 4, 1975; 1983-84 New York State Statistical Yearbook, 10 edition (S.l.: Nelson a Rockefeller Inst, 1984)